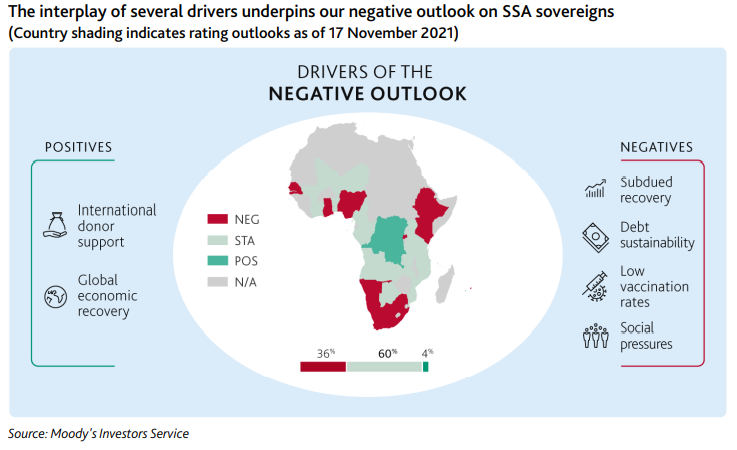

Moody's - SSA sovereign outlook is negative as the subdued economic recovery remains fragile

Our outlook for sovereign creditworthiness in 2022 in the Sub-Saharan Africa (SSA) region is

negative, reflecting our expectations of the fundamental conditions that will drive sovereign

credit over the next 12-18 months, relative to prevailing conditions in 2021. GDP growth

will only accelerate marginally in 2022, which will be insufficient to recoup the output

and income losses triggered by the pandemic. We are also likely to see scarring emerge as

support measures are gradually withdrawn.

In addition, low vaccination rates heighten the risk of renewed restrictions. The knock-on effects for already low revenue generation will keep fiscal deficits and borrowing requirements elevated next year, and debt burdens high.

Absent further international support, this will likely further weaken debt affordability and intensify liquidity pressures and external vulnerability risks, particularly given the limited

capacity of domestic banking systems to provide finance as eurobonds mature over the next

few years. At the same time, governments are likely to see social risks intensify in response to pandemic fatigue and growing demands for more fiscal support, job creation and services.

2021 overview Following a year of an unprecedented number (28) of rating actions in the SSA region in 2020, we have taken 13 actions as of 17 November as immediate liquidity pressures from the pandemic shock eased for most of the region's sovereigns.

» Long-lasting deterioration in fiscal strength drove downgrades. We downgraded Mauritius (Baa2 negative) in March after the sharp contraction in GDP and emergency pandemic spending led to a significant jump in its debt burden and weakened its fiscal strength. The tourism sector's large share of economic activity, export earnings and employment also means the lasting effects of the pandemic will continue to weigh on the recovery and slow fiscal consolidation. Botswana's (A3 stable) downgrade in April was driven by the accelerated erosion of the government's fiscal reserves, which reduced its ability to absorb future shocks.

» Some liquidity pressures will persist. We maintained Ghana's (B3 negative) outlook given the pandemic-driven increase in its borrowing and weakened debt affordability arising from its reliance on confidence-sensitive capital markets. We also maintained Kenya's (B2 negative) outlook given its lacklustre fiscal consolidation, though its IMF agreement eases immediate financing risks.

» Credit risks related to the G-20 Common Framework became clearer. We downgraded Ethiopia (Caa2 negative) twice in 2021 as the term sheet made clear that official sector lenders were intent on upholding the principle of comparable treatment for

private-sector lenders. Intensifying external liquidity pressures also increased the likelihood of losses.

» We took a few positive rating actions. We upgraded Benin (B1 stable) in March amid expectations of debt stabilisation and greater economic resiliency, and Angola (B3 stable) in September as reform implementation and a stable exchange rate, supported

by higher oil prices, improved fiscal metrics and reduced liquidity risks. We also changed Mali's (Caa1 stable) outlook to stable from negative as political conditions stabilised after the August 2020 coup. We assigned a positive rating outlook on the Democratic Republic of the Congo (Caa1 positive) in October to reflect its robust economic prospects given structural reforms.